Page 249 - Tata Chemical Annual Report_2022-2023

P. 249

Integrated Annual Report 2022-23 01-83 84-192 193-365

Integrated Report Statutory Reports Financial Statements

Standalone

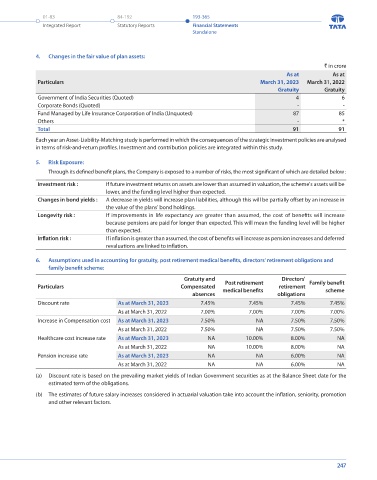

2. Changes in the fair value of plan assets: 4. Changes in the fair value of plan assets:

` in crore ` in crore

As at March 31, 2023 As at March 31, 2022 As at As at

Post Post Particulars March 31, 2023 March 31, 2022

Particulars retirement Directors' Family retirement Directors' Family Gratuity Gratuity

Gratuity retirement benefit Gratuity retirement benefit

medical medical Government of India Securities (Quoted) 4 6

benefits obligations scheme benefits obligations scheme Corporate Bonds (Quoted) - -

At the beginning of the year 91 - - - 84 - - - Fund Managed by Life Insurance Corporation of India (Unquoted) 87 85

Interest on plan assets 6 - - - 5 - - - Others - *

Employer's contributions 3 - - - 10 - - - Total 91 91

Remeasurement gain/(loss) Each year an Asset-Liability-Matching study is performed in which the consequences of the strategic investment policies are analysed

Annual return on plan assets less interest 2 - - - 2 - - - in terms of risk-and-return profiles. Investment and contribution policies are integrated within this study.

on plan assets

Benefits paid (11) - - - (10) - - - 5. Risk Exposure:

Value of plan assets at the end of the year 91 - - - 91 - - - Through its defined benefit plans, the Company is exposed to a number of risks, the most significant of which are detailed below :

(Asset)/liability (net) (5) 64 66 11 (3) 71 52 11 Investment risk : If future investment returns on assets are lower than assumed in valuation, the scheme's assets will be

lower, and the funding level higher than expected.

3. Net employee benefit expense for the year: Changes in bond yields : A decrease in yields will increase plan liabilities, although this will be partially offset by an increase in

` in crore the value of the plans' bond holdings.

Year ended March 31, 2023 Year ended March 31, 2022 Longevity risk : If improvements in life expectancy are greater than assumed, the cost of benefits will increase

Post Family Post because pensions are paid for longer than expected. This will mean the funding level will be higher

Particulars retirement Directors' retirement Directors' Family than expected.

Gratuity retirement benefit Gratuity retirement benefit Inflation risk :

medical obligations scheme medical If inflation is greater than assumed, the cost of benefits will increase as pension increases and deferred

benefits benefits obligations scheme revaluations are linked to inflation.

Current service cost 4 2 1 1 4 2 1 1 6. Assumptions used in accounting for gratuity, post retirement medical benefits, directors' retirement obligations and

Past service cost - - 13 - - - - - family benefit scheme:

Interest on defined benefit obligation (net) - 5 4 1 - 5 3 1

Components of defined benefits 4 7 18 2 4 7 4 2 Gratuity and Post retirement Directors' Family benefit

costs recognised in the Standalone Particulars Compensated medical benefits retirement scheme

Statement of Profit and Loss absences obligations

Remeasurement Discount rate As at March 31, 2023 7.45% 7.45% 7.45% 7.45%

Actuarial (gain) / loss arising from: As at March 31, 2022 7.00% 7.00% 7.00% 7.00%

- Change in financial assumptions (2) (4) (3) - (3) (6) (3) - Increase in Compensation cost As at March 31, 2023 7.50% NA 7.50% 7.50%

- Experience changes 1 (8) 2 (1) - (8) 1 - As at March 31, 2022 7.50% NA 7.50% 7.50%

Return on plan assets less interest on (2) - - - (2) - - - Healthcare cost increase rate As at March 31, 2023 NA 10.00% 8.00% NA

plan assets As at March 31, 2022 NA 10.00% 8.00% NA

Components of defined benefits costs (3) (12) (1) (1) (5) (14) (2) - Pension increase rate As at March 31, 2023 NA NA 6.00% NA

recognised in Other Comprehensive As at March 31, 2022 NA NA 6.00% NA

Income (a) Discount rate is based on the prevailing market yields of Indian Government securities as at the Balance Sheet date for the

Net benefit expense 1 (5) 17 1 (1) (7) 2 2

estimated term of the obligations.

(b) The estimates of future salary increases considered in actuarial valuation take into account the inflation, seniority, promotion

and other relevant factors.

246 247