Page 256 - Tata_Chemicals_yearly-reports-2017-18

P. 256

(iii) The Group enters into derivative financial instruments with various counterparties, principally financial institutions with investment

grade credit ratings. The fair value of derivative financial instruments is based on observable market inputs including currency spot

and forward rate, yield curves, currency volatility, credit quality of counterparties, interest rate curves and forward rate curves of the

underlying commodity etc. and use of appropriate valuation models.

(iv) The fair value of non-current borrowings carrying floating-rate of interest is not impacted due to interest rate changes, and will not

be significantly different from their carrying amounts as there is no significant change in the underlying credit risk of the Group

(since the date of inception of the loans).

(v) The fair values of the 10% unsecured redeemable non-convertible debenture (included in non-current borrowings) are derived

from quoted market prices. The Group has no other long-term borrowings with fixed-rate of interest.

(e) Financial risk management objectives

The Group is exposed to market risk (including currency risk, interest rate risk and other price risk), credit risk and liquidity risk. The Group’s

risk management strategies focus on the un-predictability of these elements and seek to minimise the potential adverse effects on its

financial performance. The Board of Directors/Committee of Board of the respective operating entities approve the risk management

policies. The implementation of these policies is the responsibility of the operating entities. The Board of Directors/Committee of Board

of the respective operating entities periodically review the exposures to financial risks, and the measures taken for risk mitigation and the

results thereof.

All hedging activities for risk management purposes are carried out by specialist teams that have the appropriate skills, experience and

supervision. The Group’s policy is not to trade in derivatives for speculative purposes.

Market risk

Market risk is the risk that the fair value of future cash flows of a financial instrument will fluctuate because of changes in market prices.

Market risk comprises three types of risk: currency risk, interest rate risk and other price risk, such as equity price risk and commodity

price risk. The value of a financial instrument may change as a result of changes in the interest rates, foreign currency exchange rates,

equity price fluctuations, commodity price, liquidity and other market changes. Financial instruments affected by market risk include

borrowings, deposits, investments and derivative financial instruments.

Foreign currency risk management

Foreign exchange risk arises on future commercial transactions and all recognised monetary assets and liabilities which are denominated

in a currency other than the functional currency of the entities of the Group. The foreign exchange risk management policy requires

operating entities to manage their foreign exchange risk against their functional currency and to meet this objective they enter into

derivatives such as foreign currency forwards, option and swap contracts, as considered appropriate and whenever necessary.

The Group has international operations and hence, it is exposed to foreign exchange risk arising from various currencies, primarily with

respect to USD. As at the end of the reporting period, the carrying amounts of the Group’s foreign currency denominated monetary

assets and liabilities, in respect to the primary foreign currency exposure i.e. USD, and derivative to hedge the foreign currency exposure

are as follows:

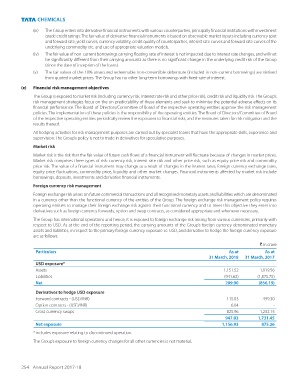

` in crore

Particulars As at As at

31 March, 2018 31 March, 2017

USD exposure*

Assets 1,151.52 1,019.56

Liabilities (941.62) (1,875.75)

Net 209.90 (856.19)

Derivatives to hedge USD exposure

Forward contracts - (USD/INR) 115.03 499.30

Option contracts - (USD/INR) 6.04 -

Cross currency swaps 825.96 1,232.15

947.03 1,731.45

Net exposure 1,156.93 875.26

* includes exposure relating to discontinued operation.

The Group’s exposure to foreign currency changes for all other currencies is not material.

254 Annual Report 2017-18