Page 188 - Tata_Chemicals_yearly-reports-2017-18

P. 188

The credit risk related to the trade receivables is mitigated by taking security deposits / bank guarantee / letter of credit - as and where

considered necessary, setting appropriate credit terms and by setting and monitoring internal limits on exposure to individual customers.

There is no substantial concentration of credit risk as the revenue and trade receivables from any of the single customer do not exceed

10% of Company revenue.

Financial instruments and cash deposits

Credit risk from balances/investments with banks and financial institutions is managed in accordance with the Company’s treasury risk

management policy. Investments of surplus funds are made only with approved counterparties and within limits assigned to each

counterparty. The limits are assigned based on corpus of investable surplus and corpus of the investment avenue. The limits are set to

minimize the concentration of risks and therefore mitigate financial loss through counterparty’s potential failure to make payments.

Financial guarantees

Financial guarantees disclosed in note 41.1(b) have been provided as corporate guarantees to financial institutions and banks that have

extended credit facilities to the Company’s subsidiaries. In this regard, the Company does not foresee any significant credit risk exposure.

Liquidity risk

Liquidity risk is the risk that the Company will not be able to meet its financial obligations as they become due. The objective of liquidity

risk management is to maintain sufficient liquidity and ensure that funds are available for use as and when required.

The Treasury Risk Management Policy includes an appropriate liquidity risk management framework for the management of the short-

term, medium-term and long term funding and cash management requirements. The Company manages the liquidity risk by maintaining

adequate cash reserves, banking facilities and reserve borrowing facilities, by continuously monitoring forecast and actual cash flows, and

by matching the maturity profiles of financial assets and liabilities. The Company invests its surplus funds in bank fixed deposit and liquid

schemes of mutual funds, which carry no/negligible mark to market risks.

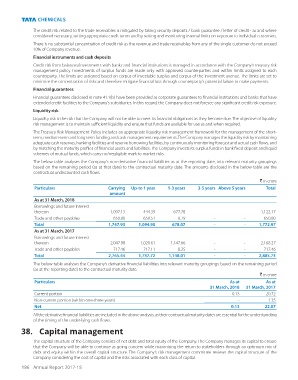

The below table analyses the Company’s non-derivative financial liabilities as at the reporting date, into relevant maturity groupings

based on the remaining period (as at that date) to the contractual maturity date. The amounts disclosed in the below table are the

contractual undiscounted cash flows.

` in crore

Particulars Carrying Up-to 1 year 1-3 years 3-5 years Above 5 years Total

amount

As at 31 March, 2018

Borrowings and future interest

thereon 1,097.13 444.39 677.78 - - 1,122.17

Trade and other payables 650.80 650.51 0.29 - - 650.80

Total 1,747.93 1,094.90 678.07 - - 1,772.97

As at 31 March, 2017

Borrowings and future interest

thereon 2,047.98 1,020.61 1,147.66 - - 2,168.27

Trade and other payables 717.46 717.11 0.35 - - 717.46

Total 2,765.44 1,737.72 1,148.01 - - 2,885.73

The below table analyses the Company’s derivative financial liabilities into relevant maturity groupings based on the remaining period

(as at the reporting date) to the contractual maturity date.

` in crore

Particulars As at As at

31 March, 2018 31 March, 2017

Current portion 0.13 20.72

Non-current portion (within one-three years) - 1.35

Net 0.13 22.07

All the derivative financial liabilities are included in the above analysis, as their contractual maturity dates are essential for the understanding

of the timing of the under-lying cash flows.

38. Capital management

The capital structure of the Company consists of net debt and total equity of the Company. The Company manages its capital to ensure

that the Company will be able to continue as going concern while maximising the return to stakeholders through an optimum mix of

debt and equity within the overall capital structure. The Company’s risk management committee reviews the capital structure of the

Company considering the cost of capital and the risks associated with each class of capital.

186 Annual Report 2017-18