Page 186 - Tata_Chemicals_yearly-reports-2017-18

P. 186

(e) Financial risk management objectives

The Company is exposed to market risk (including currency risk, interest rate risk and other price risk), credit risk and liquidity risk. The

Company’s risk management strategies focus on the un-predictability of these elements and seek to minimise the potential adverse

effects on its financial performance. The Company’s senior management which is supported by a Treasury Risk Management Group

(‘TRMG’) manages these risks. TRMG advises on financial risks and the appropriate financial risk governance framework for the Company

and provides assurance to the Company’s senior management that the Company’s financial risk activities are governed by appropriate

policies and procedures and that financial risks are identified, measured and managed in accordance with the Company’s policies and

risk objectives.

All hedging activities are carried out by specialist teams that have the appropriate skills, experience and supervision. The Company’s

policy is not to trade in derivatives for speculative purposes.

Market risk

Market risk is the risk that the fair value of future cash flows of a financial instrument will fluctuate because of changes in market prices.

Market risk comprises three types of risk: currency risk, interest rate risk and other price risk, such as equity price risk and commodity risk.

The value of a financial instrument may change as a result of changes in the interest rates, foreign currency exchange rates, equity price

fluctuations, liquidity and other market changes. Financial instruments affected by market risk include loans and borrowings, deposits,

investments and derivative financial instruments.

Foreign currency risk management

Foreign exchange risk arises on future commercial transactions and on all recognised monetary assets and liabilities, which are

denominated in a currency other than the functional currency of the Company. The Company’s management has set a policy wherein

exposure is identified, a benchmark is set and monitored closely, and accordingly suitable hedges are undertaken. The policy also includes

mandatory initial hedging requirements for exposure above a threshold.

The Company’s foreign currency exposure arises mainly from foreign exchange imports, exports and foreign currency borrowings,

primarily with respect to USD.

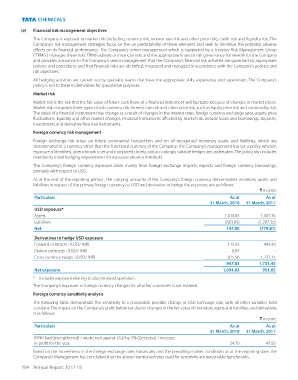

As at the end of the reporting period , the carrying amounts of the Company’s foreign currency denominated monetary assets and

liabilities in respect of the primary foreign currency i.e. USD and derivative to hedge the exposure, are as follows:

` in crore

Particulars As at As at

31 March, 2018 31 March, 2017

USD exposure*

Assets 1,010.83 1,007.76

Liabilities (863.83) (1,787.56)

Net 147.00 (779.81)

Derivatives to hedge USD exposure

Forward contracts - (USD/ INR) 115.03 499.30

Option contracts - (USD/ INR) 6.04 -

Cross currency swaps - (USD/ INR) 825.96 1,232.15

947.03 1,731.45

Net exposure 1,094.03 951.65

* includes exposure relating to discontinued operation.

The Company’s exposure to foreign currency changes for all other currencies is not material.

Foreign currency sensitivity analysis

The following table demonstrate the sensitivity to a reasonable possible change in USD exchange rate, with all other variables held

constant. The impact on the Company’s profit before tax due to changes in the fair value of monetary assets and liabilities and derivatives

is as follows:

` in crore

Particulars As at As at

31 March, 2018 31 March, 2017

If INR had (strengthened) / weakened against USD by 5% (Decrease) / increase

in profit for the year 54.70 47.58

Based on the movements in the foreign exchange rates historically and the prevailing market conditions as at the reporting date, the

Company’s Management has concluded that the above mentioned rates used for sensitivity are reasonable benchmarks.

184 Annual Report 2017-18