Page 354 - Tata Chemical Annual Report_2022-2023

P. 354

Integrated Annual Report 2022-23 01-83 84-192 193-365

Integrated Report Statutory Reports Financial Statements

Consolidated

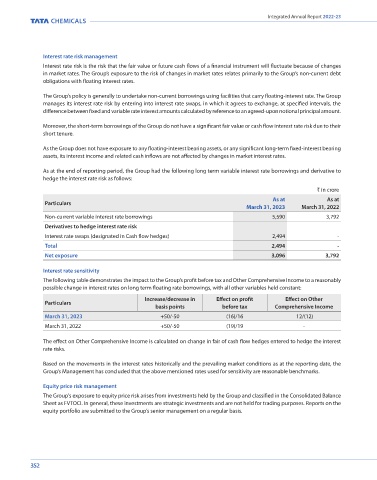

Interest rate risk management Equity price sensitivity analysis

Interest rate risk is the risk that the fair value or future cash flows of a financial instrument will fluctuate because of changes If prices of equity instrument had been 5% higher/(lower), the OCI for the year ended March 31, 2023 and 2022 would increase/

in market rates. The Group’s exposure to the risk of changes in market rates relates primarily to the Group’s non-current debt (decrease) by ` 218 crore and ` 218 crore respectively.

obligations with floating interest rates.

Commodity price risk

The Group’s policy is generally to undertake non-current borrowings using facilities that carry floating-interest rate. The Group Certain entities within the Group are affected by the volatility in the price of commodities. Its operating activities require the

manages its interest rate risk by entering into interest rate swaps, in which it agrees to exchange, at specified intervals, the ongoing production of steam and electricity and therefore require a continuous supply of fuels. Due to potential volatility in

difference between fixed and variable rate interest amounts calculated by reference to an agreed-upon notional principal amount. the price of fuels, the Group has put in place a risk management strategy whereby the cost of fuels are hedged.

Moreover, the short-term borrowings of the Group do not have a significant fair value or cash flow interest rate risk due to their Commodity price sensitivity

short tenure.

The following table shows the effect of price changes in commodities to OCI due to changes in fair value of cash flow hedges

entered to hedge commodity price risk.

As the Group does not have exposure to any floating-interest bearing assets, or any significant long-term fixed-interest bearing

assets, its interest income and related cash inflows are not affected by changes in market interest rates. ` in crore

As at As at

If the price of the future contracts were higher / (lower) by 10% Commodity

As at the end of reporting period, the Group had the following long term variable interest rate borrowings and derivative to March 31, 2023 March 31, 2022

hedge the interest rate risk as follows:

Increase / (decrease) in OCI for the year Natural gas 56/(56) 121/(121)

` in crore

As at As at Credit risk management

Particulars

March 31, 2023 March 31, 2022 Credit risk is the risk that a counterparty will not meet its obligations under a financial instrument or customer contract, leading

Non-current variable interest rate borrowings 5,590 3,792 to a financial loss. The Group is exposed to credit risk from its operating activities, primarily trade and other receivables and

from its investing activities, including Loans given, deposits with banks and financial institutions, investment in mutual funds

Derivatives to hedge interest rate risk

and other financial instruments.

Interest rate swaps (designated in Cash flow hedges) 2,494 -

Total 2,494 - The carrying amount of financial assets represents the maximum credit exposure, being the total of the carrying amount of

balances with banks, short term investment, trade receivables and other financial assets excluding equity investments.

Net exposure 3,096 3,792

The Group considers a financial asset to be in default when:

Interest rate sensitivity

- the debtor is unlikely to pay its credit obligations to the Company in full, without recourse actions such as security realizations, etc.

The following table demonstrates the impact to the Group’s profit before tax and Other Comprehensive Income to a reasonably

possible change in interest rates on long term floating rate borrowings, with all other variables held constant: - the financial asset is 120 days past due.

Increase/decrease in Effect on profit Effect on Other

Particulars Trade and other receivables

basis points before tax Comprehensive Income

The Trade and other receivables of Group are majorly unsecured and derived from sales made to a large number of independent

March 31, 2023 +50/-50 (16)/16 12/(12) customers. Customer credit risk is managed by each business unit subject to the established policy, procedures and control

March 31, 2022 +50/-50 (19)/19 - relating to customer credit risk management. Before accepting any new customer, the Group has appropriate level of control

procedures to assess the potential customer's credit quality. The credit-worthiness of its customers are reviewed based on their

The effect on Other Comprehensive Income is calculated on change in fair of cash flow hedges entered to hedge the interest financial position, past experience and other factors. The credit period provided by the Group to its customers generally ranges

rate risks. from 0-60 days. Outstanding customer receivables are regularly monitored. Provision is made based on expected credit loss

method or specific identification method.

Based on the movements in the interest rates historically and the prevailing market conditions as at the reporting date, the

Group’s Management has concluded that the above mentioned rates used for sensitivity are reasonable benchmarks. The credit risk related to the trade receivables is mitigated by taking security deposits / bank guarantee / letter of credit - as and

where considered necessary, setting appropriate payment terms and credit period, and by setting and monitoring internal limits

Equity price risk management on exposure to individual customers.

The Group's exposure to equity price risk arises from investments held by the Group and classified in the Consolidated Balance

Sheet as FVTOCI. In general, these investments are strategic investments and are not held for trading purposes. Reports on the As the revenue and trade receivables from any of the single customer do not exceed 10% of Group revenue, there is no substantial

equity portfolio are submitted to the Group’s senior management on a regular basis. concentration of credit risk, except as disclosed in note 41.1(d).

For certain other receivables, where recoveries are expected beyond twelve months of the balance sheet date, the time value

of money is appropriately considered in determining the carrying amount of such receivables.

352 353